503 991 5453

Payroll and employee paycheck tax withholdings: mistakes that can lead to penalties, interest, and personal liability

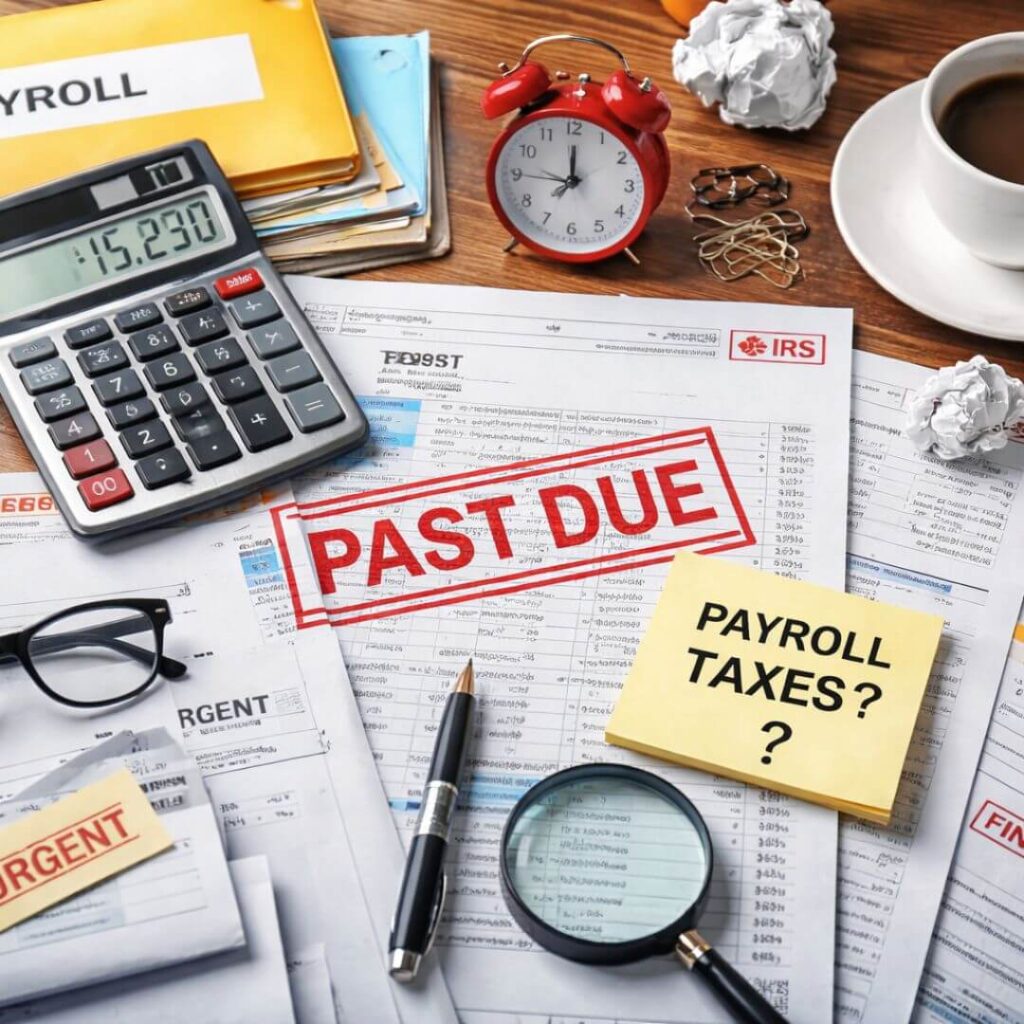

Running a business involves many responsibilities, but few are as sensitive as handling payroll. It is not just about paying wages. It also involves properly withholding, reporting, and paying the taxes related to those wages.

Many business owners, especially small business owners, make mistakes that seem minor but can quickly escalate into penalties, interest, official notices, and even personal liability. One of the most serious problems occurs when a business withholds taxes from an employee’s paycheck but does not remit them to the proper authority on time. The IRS considers those amounts to be funds held in trust, not money available for the business to use.

In this article, we explain the most common payroll mistakes, the real consequences that may arise, the key deadlines you need to monitor, and the steps you can take to avoid these types of problems.

Why is payroll such a sensitive issue?

When a business pays its employees, it is not just covering wages. Tax obligations are also involved, and they must be handled accurately. These include federal income tax withholding, Social Security and Medicare taxes, as well as state payroll-related obligations.

The key point is this: part of the money withheld from the employee does not belong to the business. That amount was deducted in order to be paid to the appropriate authority. When the employer uses it to cover other expenses or simply allows time to pass without making the payment, the issue stops being a simple administrative mistake and becomes a serious compliance failure. The IRS may impose penalties for failing to deposit employment taxes on time, in the correct amount, or through the proper method.

Common payroll mistakes that cause serious problems

1) Withholding employee taxes and not paying them on time

This is one of the most serious mistakes. Sometimes a business experiences cash flow problems and decides to temporarily use that money to cover rent, suppliers, inventory, or urgent expenses. The reasoning is usually the same: it will be replaced later.

The problem is that this money should not be touched. When taxes are withheld from employees and not remitted on time, the consequences can go far beyond a fine. In certain cases, the IRS may seek direct liability against the person responsible for handling those funds.

2) Depositing payroll taxes late

Some business owners calculate payroll correctly but fail to meet the deposit deadline. That also creates problems. It is not enough to intend to pay; payment must be made within the applicable deadline.

Federal penalties for late deposits can accumulate, and the financial impact increases if the delay happens repeatedly or if there are already outstanding balances.

3) Filing forms but not sending the corresponding payment

Another common mistake is filing the reports but leaving the payment for later. This creates a false sense of compliance. Even if the form has been filed, the debt still exists and can continue to grow with penalties and interest.

4) Neglecting state payroll-related obligations

In addition to federal obligations, employers must also comply with state payroll-related reporting and payment requirements. In Oregon, there are specific obligations administered through the combined payroll reporting and payment system. When those reports or payments are filed late, penalties may also apply. The 2026 state guide indicates, for certain payroll forms, a 5% penalty for late payment and an additional 20% penalty for filing more than one month late.

5) Operating without a calendar or internal controls

Many problems do not begin with bad faith, but with disorganization. There are no visible deadlines, no reminders, no payment reconciliation, and no one verifies whether the correct deposit was actually made. Over time, that lack of organization turns into delays, discrepancies, notices, and financial stress.

Real consequences of poor payroll management

- Penalties and interest. The first consequence is usually financial. When deposits or payments are not made correctly, penalties and interest begin to accumulate. What seemed like a small delay can become a much harder debt to control. The impact does not just affect accounting; it directly affects the business’s cash flow.

- Official notices and collection pressure. When noncompliance continues, letters and demands begin to arrive. These notices consume time, create stress, and force the business to dedicate resources to fixing problems that could have been avoided with better controls.

- Operational and financial risk. Poorly managed payroll does not just create a tax problem. It also reflects a lack of administrative structure. A business that does not properly control its deadlines and payments runs a greater risk of making other mistakes, losing visibility into its cash flow, and making reactive decisions.

- Personal liability. This is the most delicate point. Many people believe the problem stays within the company, but that is not always the case. If the business does not remit the withheld taxes, the IRS may impose the Trust Fund Recovery Penalty on the responsible person. In addition, the IRS manual states that the willful failure to collect or pay over those taxes may constitute a criminal offense under 26 USC 7202.

This means that when taxes are withheld and not remitted, the risk can shift from the business to the individual who had the duty to properly handle those payments.

Important deadlines you need to keep in mind

One of the best ways to prevent payroll problems is to clearly understand your compliance deadlines.

- Federal payroll tax deposits. The exact due date depends on the deposit schedule assigned to the employer. In general terms, many businesses fall into one of these categories:

- Monthly depositor. The deposit is generally due on the 15th day of the month following the payroll date.

- Semi-weekly depositor. If wages were paid on Wednesday, Thursday, or Friday, the deposit is generally due the following Wednesday. If wages were paid on Saturday, Sunday, Monday, or Tuesday, the deposit is generally due the following Friday.

- Form 941. This form is filed quarterly. The most common deadlines are:

1) April 30

2) July 31

3) October 31

4) January 31 - Forms W-2 and W-3. Delivery to the employee and the corresponding filing are generally due on January 31.

State payroll reports

In Oregon, quarterly combined payroll-related reports generally follow these deadlines:

- April 30

- July 31

- October 31

- January 31

Failing to keep track of these deadlines is one of the most common reasons businesses end up paying more penalties and interest.

How can you prevent these problems?

Prevention begins with one simple idea: payroll cannot be handled improvisationally.

First, it is essential to separate, both mentally and operationally, the money withheld from employees. It should not be mixed with funds available for other business expenses. Second, business needs a clear compliance calendar, with reminders and real follow-up. Third, deposits must be verified to ensure they are made correctly, in the proper amount, and on time.

Finally, professional support is advisable when the business does not have the internal capacity to manage these processes accurately.

Many business owners do not get into trouble because they intend to be noncompliant. They get into trouble because they underestimate how sensitive payroll is, let deadlines pass, or make short-term cash flow decisions that end up costing much more later.

La meta no es pagar más, es pagar con control

Payroll problems do not necessarily begin with fraud or bad intentions. Many times, they begin with disorganization, lack of control, or the belief that a small delay can be fixed later. But when it comes to taxes withheld from an employee’s paycheck, the situation becomes especially sensitive.

Failing to pay on time can lead to penalties, interest, official notices, and collection pressure. And when withholdings are not remitted, the problem can escalate all the way to personal liability.

For that reason, payroll should not be viewed as a simple administrative task. It must be managed with structure, control, and timely compliance.

At Grupo Contable, we can help you review your payroll, organize your deadlines, correct your processes, and reduce the risk of costly mistakes. If you want to avoid penalties, interest, and bigger problems, contact us today.